Most people shopping for a lease spend a lot of energy on the monthly payment.

Makes sense — that’s the number that hits your bank account every month.

But if you really want to understand whether a lease deal is good or bad, there’s a number hiding deeper in the contract that deserves a lot more attention: the residual value.

Once you understand how residuals work, you’ll never look at a lease the same way again.

In This Post

- So, What Exactly Is a Residual Value?

- How Is the Residual Determined?

- Residual vs. Depreciation: Two Sides of the Same Coin

- Why a High Residual Is (Usually) Great News

- When a High Residual Can Work Against You

- Residual and Mileage: A Direct Relationship

- Questions to Ask Your Finance Manager About the Residual

- The Bottom Line

- Frequently Asked Questions

- References

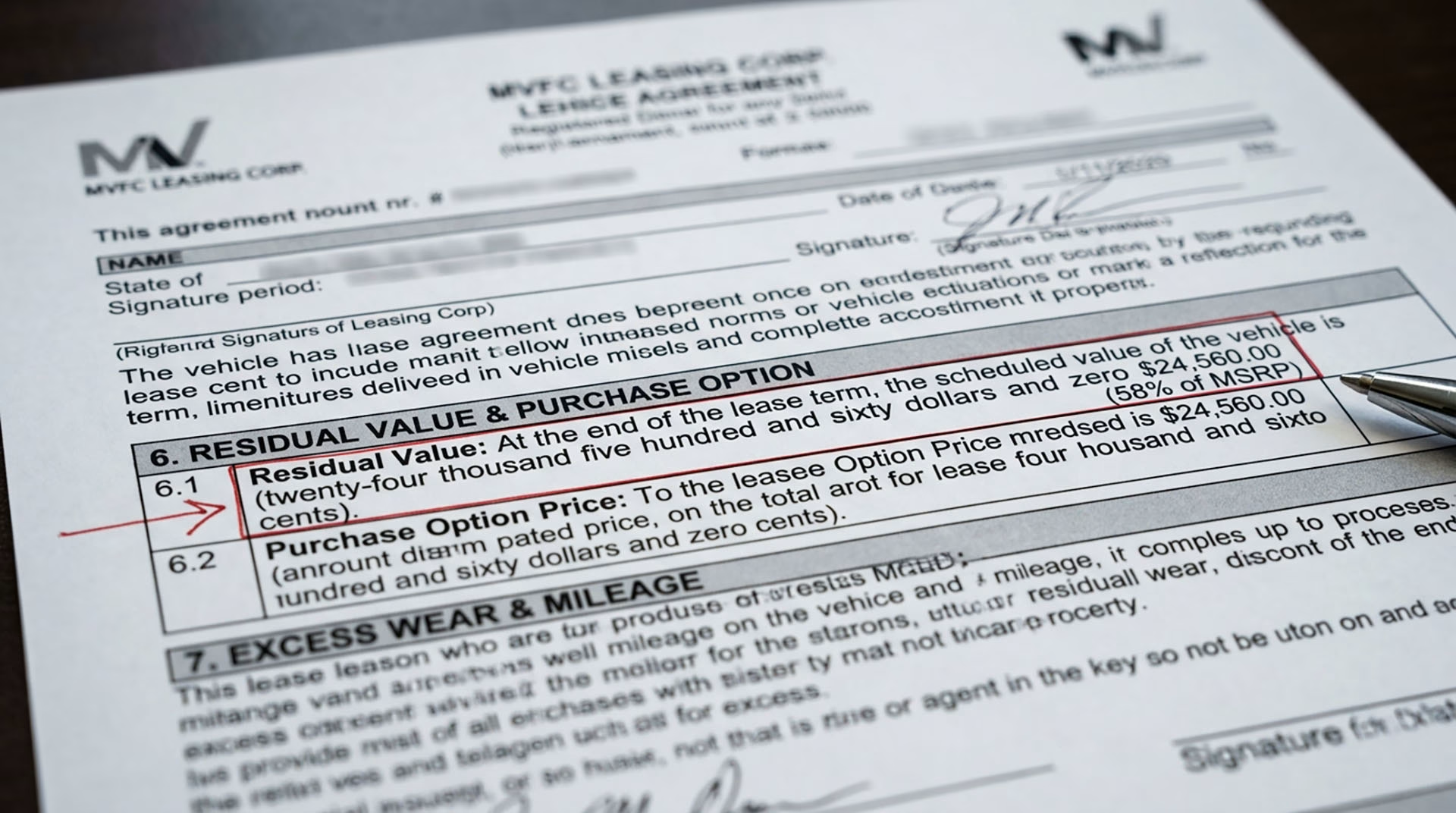

So, What Exactly Is a Residual Value?

The residual value (sometimes called the “residual amount” or “lease-end value”) is the estimated worth of the vehicle at the end of your lease term. It’s set by the lender — usually the automaker’s captive finance arm — before you ever sign anything, and it’s expressed either as a dollar amount or a percentage of the vehicle’s MSRP.

Here’s the simple version: when you lease a car, you’re essentially paying for the portion of the car’s value that gets used up during your lease term — not the whole thing. The residual is what’s left over.

Example:

- MSRP: $45,000

- Residual at 36 months: 55% → $24,750

- You’re financing: $45,000 − $24,750 = $20,250 (plus fees and interest)

That $20,250 is the “depreciation” portion you’re paying for over three years. The residual is the chunk you’re not paying for — which is exactly why a higher residual means lower monthly payments.

How Is the Residual Determined?

You don’t get to pick your residual. It’s set by the financing institution based on a mix of data and projection:

- Historical resale data — What have similar vehicles sold for at auction after lease returns?

- Mileage allowance — Higher annual mileage = more wear = lower residual

- Lease term — Longer terms typically mean lower residuals (more depreciation)

- Market demand — Trucks and SUVs with strong resale history often earn higher residuals

- Incentive programs — Automakers sometimes artificially inflate residuals to make monthly payments more attractive during promotional periods

Third-party guides like ALG (Automotive Lease Guide) publish residual predictions that lenders use as benchmarks. Brands like Toyota, Honda, and Subaru tend to consistently earn higher residuals because their vehicles hold value well on the used market.

Residual vs. Depreciation: Two Sides of the Same Coin

It helps to think of residual and depreciation as opposite ends of a see-saw. When one goes up, the other goes down — and that directly affects what you pay.

| Residual Value | Depreciation You Pay | Monthly Payment Impact |

|---|---|---|

| High (60%+) | Low | Lower payments |

| Average (45–55%) | Moderate | Mid-range payments |

| Low (below 40%) | High | Higher payments |

This is why leasing a Toyota Camry often makes more financial sense than leasing a comparable domestic sedan — not because the Camry is necessarily cheaper, but because Toyota’s strong resale history supports higher residuals, which means less depreciation to fund each month.

Why a High Residual Is (Usually) Great News

A high residual value works in your favor in a few important ways:

- Lower monthly payments — You’re only financing the depreciation, so less depreciation = less to pay

- More car for your money — You may be able to afford a higher trim level than you expected

- Better value on short-term leases — Vehicles with high residuals depreciate least in the first 2–3 years, which is exactly the lease window

Popular vehicles with historically strong residuals include:

- Toyota Tacoma and 4Runner

- Jeep Wrangler (one of the rare domestic vehicles with standout residuals)

- Honda CR-V and Pilot

- Subaru Outback and Forester

- Ram 1500 (particularly well-supported residuals through Ram Financial)

When a High Residual Can Work Against You

This is the part most people never think about — and it matters a lot if you’re considering buying the vehicle at lease end.

When you buy out a lease, you pay the residual value (plus applicable taxes and fees). If the residual was set artificially high — meaning the car is actually worth less on the open market at that point — you’d be overpaying to keep it.

Three scenarios to understand:

| Situation | What It Means for You |

|---|---|

| Market value > Residual | Great buyout deal — you have built-in equity |

| Market value ≈ Residual | Fair buyout, roughly what you’d pay elsewhere |

| Market value < Residual | Overpaying to buy — better to return the vehicle |

During the pandemic and in the years following, used car prices skyrocketed. Millions of lessees found themselves sitting on vehicles worth significantly more than the residual — meaning they had real equity in a leased car. Some sold those buyout rights to dealers for a profit. That’s how unusual the market became, and it’s a perfect illustration of why tracking residual vs. market value matters.

Residual and Mileage: A Direct Relationship

One of the most straightforward ways residuals get adjusted is through mileage. Lenders offer several standard mileage tiers, and each one comes with a corresponding residual:

- 10,000 miles/year — Highest residual (car is used less, worth more at return)

- 12,000 miles/year — Standard, most common option

- 15,000 miles/year — Lower residual (more wear expected)

If you drive a lot, it may seem tempting to just take the lower-mileage lease and pay the overage later. Do the math first — overage charges typically run $0.15–$0.25 per mile, which adds up fast. But going to a higher mileage option upfront will lower your residual and raise your payment. There’s usually a break-even point, and it’s worth calculating before you sign.

Questions to Ask Your Finance Manager About the Residual

Before you sign a lease, make sure you have clear answers to these:

- What is the residual value in dollars — not just as a percentage?

- Is this residual based on a manufacturer-subsidized program or standard lender guidelines?

- How does the residual change if I choose a higher mileage tier?

- Is the residual guaranteed, regardless of what the car is actually worth at lease end?

- What is the purchase option process if I want to buy at the end?

A good finance manager won’t hesitate to walk you through all of these. If someone is evasive about the residual, that’s a red flag.

The Bottom Line

Residual value isn’t the flashiest part of a lease conversation, but it might be the most important one. It determines how much of the vehicle’s depreciation you’re responsible for, it shapes your monthly payment, and it sets the terms for a potential buyout. Understanding it gives you leverage — both in evaluating whether a lease makes sense and in comparing deals across different vehicles and brands.

Next time you’re looking at a lease, don’t just ask “what’s the payment?” Ask: “What’s the residual, and what’s the MSRP it’s based on?” Those two numbers will tell you almost everything you need to know.

Frequently Asked Questions

Q: Can I negotiate the residual value? No. The residual is set by the lender and is non-negotiable. What you can negotiate are the selling price (capitalized cost), the money factor, and any fees rolled into the deal. Lowering the cap cost effectively lowers your payment even if the residual stays the same.

Q: What happens if my car is worth more than the residual at lease end? You have equity. You can buy the vehicle at the residual price (a below-market deal), or in some cases sell or transfer that buyout right to a third party. Not all leasing companies allow third-party buyouts, so check your contract.

Q: What happens if my car is worth less than the residual at lease end? If you’re returning the vehicle, nothing — that’s the lender’s risk to absorb, not yours. If you want to buy it, you’d be paying more than market value, so you’re better off returning it and shopping elsewhere.

Q: Is a higher residual always better? For monthly payments, yes. For buyouts, it depends on the market. A very high residual can make buying the vehicle at lease end expensive if market values have dropped.

Q: Does the residual change if I put money down? No. A cap cost reduction (down payment) lowers the amount you’re financing, but the residual stays the same. It’s always based on a percentage of MSRP regardless of how much you put down upfront.

Q: Does the money factor affect the residual? No. The money factor (lease interest rate) and the residual are separate variables. Both affect your monthly payment, but they’re independent of each other.

Q: What is a “subsidized” residual? When an automaker wants to move inventory or push a specific model, they’ll instruct their captive finance company to set the residual higher than market data would support. This artificially lowers your monthly payment. It’s a marketing tool — and it can be a genuinely great deal for the consumer, as long as you’re not planning to buy the vehicle at the end.

References

- Automotive Lease Guide (ALG) — Industry benchmark for residual value forecasting: www.alg.com

- Consumer Financial Protection Bureau — Auto Leasing Overview: www.consumerfinance.gov

- Federal Reserve — Consumer Leasing Act (Regulation M): www.federalreserve.gov/releases/g20/

- Edmunds — True Cost to Own & Lease Calculators: www.edmunds.com

- Kelly Blue Book — Residual Value and Lease Education Center: www.kbb.com

- LeaseHackr — Community resource for lease deal analysis and money factor/residual data: www.leasehackr.com